The Global liquefied natural gas LNG Market

As economic analyses showed, transporting liquefied natural gas (LNG) by sea is more competitive compared to gas pipelines, using LNG carriers to bring the gas from its production areas to the plants, where it’s returned to a usable gaseous state. Once liquefied, its volume is about 1/600th of the volume of natural gas, thus making it possible to transport it in enormous quantities. During the liquefaction process, the gas is cooled to around -160 °C and its impurities, such as oxygen, carbon dioxide, sulphur and water, are removed; the LNG becomes odourless, colourless, non-toxic, non-corrosive and non-flammable.

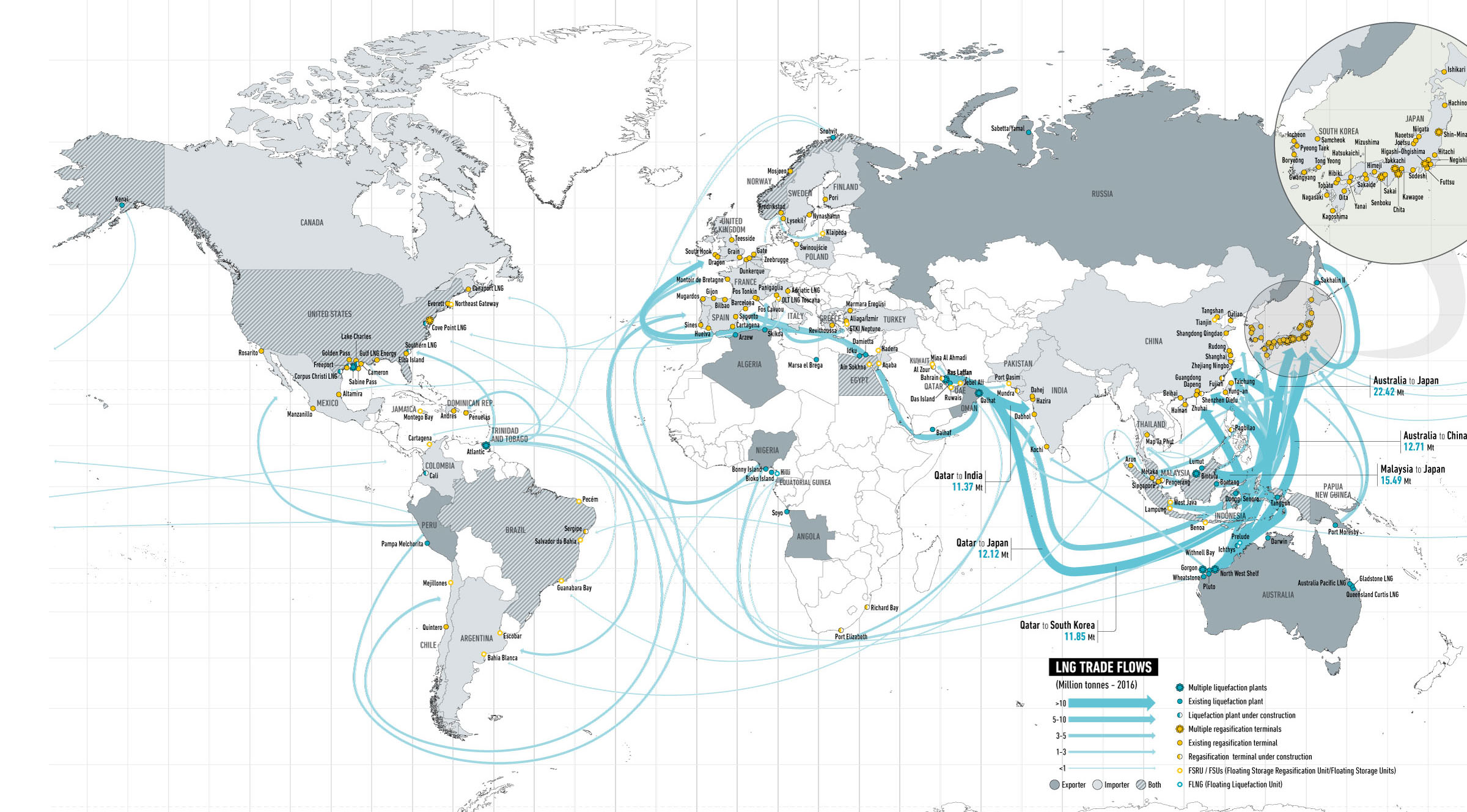

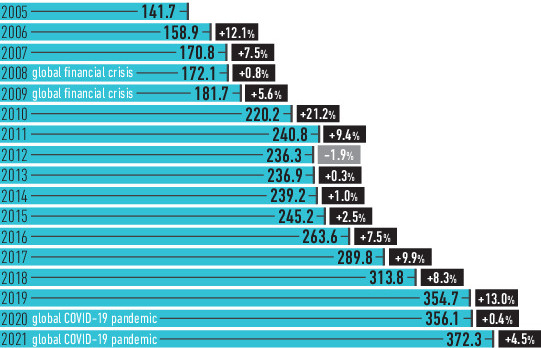

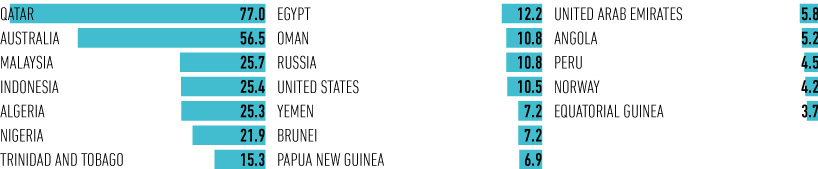

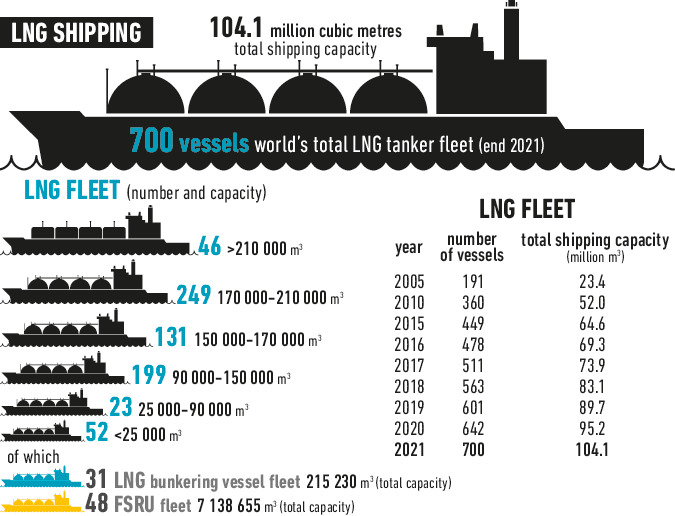

LNG is in constant growth and increasingly globalized, and LNG-related technologies are currently undergoing major developments. The various production phases (liquefaction, sea transport of LNG, regasification and transfer to the end users) are constantly being observed by managing companies: LNG trains, LNG carriers and regasification plants are always being perfected from a technical, economic and safety standpoint.

Infrastructures continue to increase both on land and in the sea. There has been a boom in FSRUs (Floating Storage and Regasification Units) since 2015, which for emerging countries represent an excellent solution for importing natural gas, as they are half the cost of onshore regasification plants, faster to deploy, and they can be easily relocated to meet changing demand. The impact of the Russia-Ukraine conflict that began in February 2022 has driven more project uptakes of new LNG receiving terminals, including many FSRUs, across coastal Europe, to replace imports from Russian pipelines, diversify supply and strengthen energy security.

- GIIGNL (International Group of Liquefied Natural Gas Importers), Annual Report (various editions);

- IGU (International Gas Union), World LNG Report 2022;